Michigan property taxes often seem like an enigma, leaving homeowners and potential buyers grappling with questions about how much they truly owe and why the amounts vary so widely. In this state, the complexity arises from a unique combination of valuation methods, tax caps, local millage rates, and exemptions that interact to determine your bill. A Michigan property tax estimator isn’t just a number-crunching tool—it’s an essential asset that demystifies these layers, offering you clarity and control over a substantial financial obligation. For investors analyzing rental property yields, first-time buyers budgeting for their dream home, or long-term owners preparing for reassessment seasons, mastering this tool can reveal insights that save thousands.

What sets Michigan’s property tax landscape apart is the Proposal A system, which dampens tax increases for existing homeowners but can produce sharp surprises for new buyers or those who have made significant property improvements. Understanding the estimator involves grasping terms like State Equalized Value (SEV), taxable value, and the local millage rate that together shape your tax bill. With a reliable Michigan property tax calculator, you can simulate scenarios, compare neighborhoods, and forecast tax trends well before the official bills arrive. This foresight helps reduce surprises, plan strategically, and sometimes challenge assessments that don’t align with fair market realities.

Whether you are assessing a $350,000 suburban home near Grand Rapids or a lakeside property with varied tax levies, using an estimator correctly is not just about plugging numbers—it requires understanding the underlying mechanics and local contexts. This article navigates you through those intricacies, empowering you to estimate property taxes not by guesswork, but with confidence and precision.

Key takeaways:

- Michigan’s property tax system uses a capped taxable value reflecting market changes, creating complexity behind your tax bill.

- Local millage rates vary drastically by school district and municipality, making location a major driver of your tax burden.

- Using an online property tax estimator effectively involves understanding input values like SEV and exemptions such as the Principal Residence Exemption.

- Reviewing your tax assessment yearly, and knowing when and how to appeal, can reduce your property tax liabilities.

- Strategic insights like homestead exemptions and agricultural classification provide meaningful tax relief opportunities for qualifying homeowners.

How Michigan’s Property Tax System Works: The Foundation of Accurate Estimation

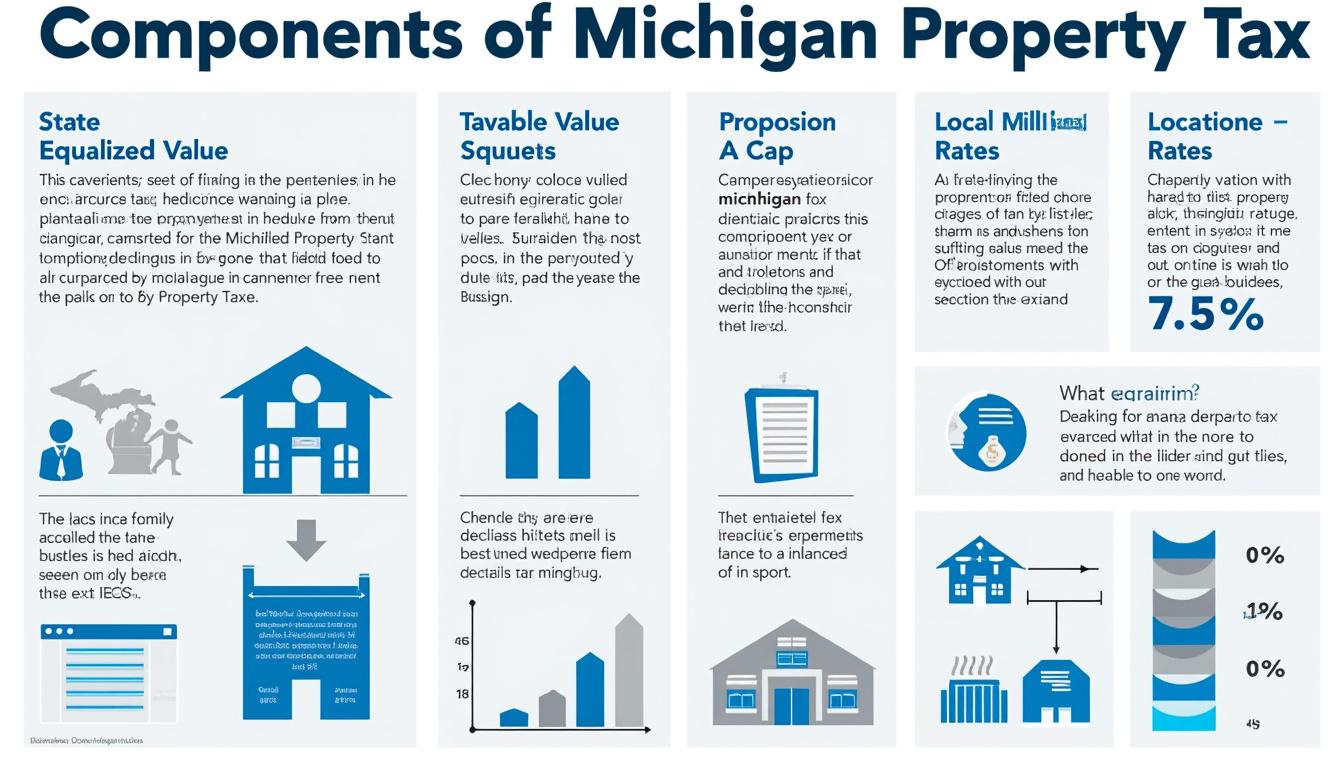

Michigan’s property tax structure is unlike many other states due to its unique formula combining market valuation, legally capped taxable values, and varying millage rates. At the core, your property is first assessed based on its market value, or what it would likely sell for under normal conditions. This assessed value, often termed the State Equalized Value (SEV), is the starting point for tax calculations but is not the final taxable amount on your bill.

The key difference shaping Michigan’s landscape is Proposal A, passed in 1994, which limits the increase of taxable value each year to no more than 5%. This provision ensures that even if the market surges dramatically, your taxable value—and thus tax obligation—increases only modestly during ownership. However, when a property changes hands, the taxable value resets to the full market value assessment. This reset explains why new buyers often face a sudden spike in taxes compared to previous owners.

The actual property tax you owe is calculated by multiplying your taxable value by the local millage rate, which is the tax rate expressed as mills per $1,000 of taxable value. Each taxing authority—school districts, counties, cities, and other local entities—sets its millage, resulting in a cumulative tax rate that can vary widely by neighborhood. For instance, a home in a well-funded school district with extensive services may face a 28-mill combined rate, while a rural township might have a significantly lower total millage. This local variability is a major reason why a Michigan property tax calculator incorporating accurate millage data is indispensable for precise estimates.

Understanding this system helps elucidate why your property tax bill rarely reflects simply a flat percentage of your home’s market price. Instead, it’s the interplay between your capped taxable value and the sum of millage rates that gives you the final figure, explaining the sometimes puzzling fluctuations in year-over-year bills. By factoring in the Principal Residence Exemption (PRE), which reduces school operating taxes for primary residents, and knowing your property classification, the system’s complexity becomes manageable.

Benefits and Limitations of Michigan Property Tax Calculators

A Michigan property tax calculator is your ally for navigating this intricate system efficiently. The tool automates the complex math involving capped values, multiple millage rates, and exemptions. Rather than manually looking up tax rates or guessing the effect of Proposal A, the calculator consolidates these factors to produce an accurate estimate tailored to your property and location. It allows prospective buyers and current owners alike to explore « what if » scenarios, such as comparing tax burdens across school districts or projecting future increases.

For example, a potential buyer considering two homes—one in a high millage district and another in a lower one—can use a property tax estimator to see the actual annual tax differences, which often outweigh the purchase price differential when accumulated over years. Similarly, investors evaluating rental properties can precisely gauge carrying costs to influence their investment calculations.

However, not all online estimators are created equal. Some provide only rough approximations using average tax rates and omit state-specific adjustments like taxable value caps or exemptions. An effective Michigan property tax calculator needs to incorporate:

- State Equalized Value (SEV): The estimated market value determined by assessors.

- Taxable Value: Calculated using Proposal A rules, typically capped or reset after ownership changes.

- Millage Rates: Specific to each city, township, and school district, reflecting the combined local tax burden.

- Exemptions: Specifically the Homestead or Principal Residence Exemption and other relevant deductions.

Fortunately, resources such as the Michigan property tax calculator on PaycheckAdvisor and official government tools at Michigan’s Treasury Department estimator provide the necessary data integration for precise results.

Limitations arise because appraised market values can fluctuate, and local millage rates might change year to year, reflecting voter-approved levies or municipal budgets. Calculators give a snapshot estimate but need up-to-date inputs and careful interpretation, especially around unique cases such as newly improved properties, inherited assets, or those under agricultural classification.

Step-by-Step Guide on Using a Michigan Property Tax Estimator Effectively

Knowing the mechanics is crucial, but putting this knowledge into practice means mastering the estimator tools correctly. Here’s a clear, actionable roadmap for using a Michigan property tax calculator to its full potential:

- Identify the Market Value or SEV: Gather your property’s current market value through trusted listing sites like Zillow or your local assessor’s office. For future purchases, use the expected sale price; for current owners, use your latest assessed value.

- Find Your Local Millage Rates: Check your city or township’s official website or latest tax bill to note the millage rates for all local taxing authorities (school district, county, city). These rates can vary greatly even between neighboring areas.

- Understand Your Taxable Value Status: If you own the property, taxable value is capped annually (max 5% increase). For new buyers, it resets to market value in the first year, impacting the estimate significantly.

- Apply Homestead or Other Exemptions: If you qualify for the Principal Residence Exemption, specify the percentage claimed to reduce school operating taxes accordingly.

- Input Your Data into the Calculator: Use a reliable tool such as the Grand Rapids property tax estimator to input your values and location.

- Analyze the Output: Review the breakdown of tax amounts by taxing units and compare the estimated yearly bill to previous years to spot anomalies or anticipate changes.

- Experiment with Scenarios: Adjust market values and exemption percentages to simulate potential changes or compare multiple properties swiftly.

For instance, if you’re considering buying a $400,000 home with a 28-mill combined rate, your first-year taxable value is $400,000, resulting in a property tax close to $11,200. Under Proposal A, if the taxable value grows only by 5% the following year, your tax jumps to about $11,760. Estimators help you plan for such increases in advance and avoid budget shocks.

Understanding Key Variables That Influence Your Michigan Property Tax Bill

The final property tax figure is a product of many intertwined factors, and grasping these helps you interpret estimator outputs and plan accordingly.

School District Millage Rates

Schools often set the largest chunk of your property tax rate. With rates fluctuating from 18 to 22 mills in many parts of Michigan, this single variable can mean thousands of dollars difference over a homeowner’s tenure. Choosing a home just inside one district versus another can change your tax bill by several hundred dollars annually.

Municipal and County Taxes

Local government needs—roads, public safety, libraries—are funded through additional millage rates layered on top of school taxes. Urban areas tend to have higher municipal rates, while rural areas may pay less but receive fewer services. This distinction can change after-tax budget reports dramatically.

Assessments Triggered by Improvements

Major renovations or additions can trigger reassessment, resetting your taxable value closer to market price despite the 5% annual increase cap. If planning extensive remodeling, anticipate a one-time tax increase and factor that into your investment calculations.

Homestead vs. Non-Homestead Status

Claiming the Principal Residence Exemption reduces school operating tax millage significantly. Rental or vacation properties lacking the exemption are taxed at higher rates, sometimes up to 50% more. This difference matters when buying investment properties or second homes.

Agricultural Classification

Property used for qualifying agricultural purposes may register under a different classification, lowering the millage rate. For rural homeowners utilizing more than two acres for farming, orchards, or vineyards, this status saves on costs each year but requires verified compliance with state criteria.

Local Millage Elections and Levies

Voters occasionally approve increased millage rates for specific projects. Such elections can raise your annual taxes with little warning, so staying informed with local government calendars keeps you prepared.

| Factor | Effect on Property Tax | Typical Range | Example Impact Over 10 Years |

|---|---|---|---|

| School District Millage Rate | Highest influence on total tax | 18 – 22 mills | +$20,000 to tax bill |

| Municipal taxes | Varies by city/township | 3 – 10 mills | +$5,000 |

| Proposal A Cap | Limits yearly increase to 5% | Max 5%/year growth | Reduces tax spikes after market growth |

| Homestead Exemption | Reduces school operating tax burden | 60,000 – 80,000 taxable value exempted | -$15,000 to $20,000 taxes saved |

| Agricultural Classification | Potential lower millage rate | Varies by county | Significant savings for qualifying landowners |

How Homestead Exemptions and Tax Relief Programs Can Reduce Your Michigan Property Taxes

The Principal Residence Exemption (PRE), commonly known as the homestead exemption, is a pivotal tool in Michigan’s property tax landscape. It exempts a set amount of a primary residence’s taxable value from the school operating millage taxes, typically between $60,000 and $80,000. This equates to substantial annual savings—around $1,500 a year for a home with a 20-mill school rate on a $400,000 taxable value.

Claiming the exemption requires filing an affidavit with the local assessor’s office, and it applies only if you occupy the home as your primary residence. Properties partially rented out or classified as multi-dwelling may receive a prorated exemption. Failure to renew or notify changes can result in penalties and retroactive taxes, so keeping your status current is essential.

Additionally, Michigan offers specific tax relief programs for seniors, disabled persons, and disabled veterans. The Property Tax Deferral Program, for instance, allows eligible seniors and disabled homeowners with limited incomes to defer property taxes until the property is sold or transferred, reducing immediate financial stress.

Veterans with qualifying disabilities can obtain exemptions that eliminate school operating taxes altogether, a benefit often overlooked but significant. Recognizing and utilizing these programs effectively can meaningfully reduce your annual tax bill and contribute to long-term affordability.

Beyond exemptions, savvy homeowners also consider strategic approaches like timing home purchases to optimize proration on tax payments or exploring agricultural classifications if applicable. Using these methods in tandem with an accurate property tax estimator provides a powerful toolkit for managing Michigan property taxes.